7 Questions Your Financial Advisor Should Be Able to Answer About Crypto

I recently reached out to a dozen financial advisors in my area to talk about crypto. One agreed to have the conversation.

Just one.

A few years ago, I tried the same thing with about thirty advisors.

Two were willing to engage. So the ratio is improving (barely 🤣 ) but the gap between client interest and advisor readiness is still enormous.

Here is the thing though, the advisors themselves are coming around.

According to the Bitwise/VettaFi 2026 Benchmark Survey:

56% of financial advisors now personally own digital assets.

32% are allocating to crypto in client accounts (up from 22% in 2024).

94% of advisors report that clients have asked about crypto in the past year.

The demand is there. The personal conviction is forming.

But the professional infrastructure to act on it? That is still catching up. A separate CoinShares survey found:

62% of advisors say recommending Bitcoin does not align with their fiduciary duty.

And yet, 91% of those same advisors are optimistic about Bitcoin’s mainstream adoption.

That is a striking disconnect. The belief is ahead of the behavior.

This is not a hit piece on financial advisors. Most are smart, credentialed professionals doing right by their clients. But digital assets represent an entirely new category of investable opportunity, and the industry has been slow to build competency around it.

So here is the question that matters: is your advisor asleep at the wheel, or do they just need better tools?

The following seven questions will help you figure that out. Bring them to your next meeting. The answers will tell you a lot.

The 7 Questions

1. How do you think about crypto in a portfolio: speculative trade or strategic asset class?

This is the foundational question. You want to understand whether your advisor views digital assets as gambling chips, venture-style bets, digital commodities, or infrastructure investments.

Each of those frameworks leads to different allocation decisions, risk management approaches, and timelines.

If the answer is some version of “it’s all speculation,” that is a red flag.

Not because speculation doesn’t exist in crypto (it absolutely does), but because lumping every digital asset into a single bucket signals a lack of nuance.

Bitcoin, Ethereum, stablecoins, and altcoins are fundamentally different instruments with different risk profiles. A good advisor should be able to articulate the distinction.

2. What allocation range would you recommend, and what drives that number?

Push for specifics here.

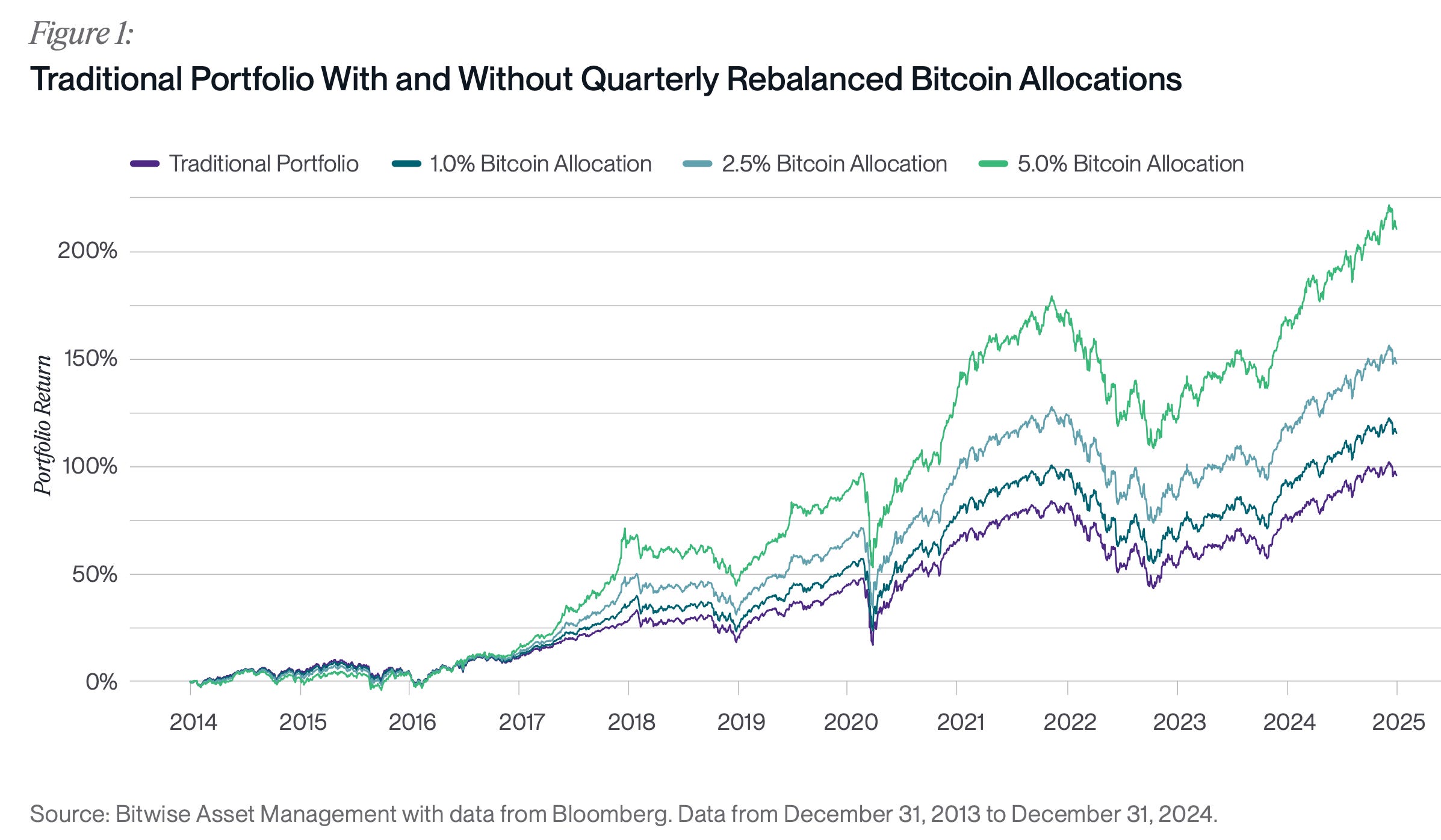

Over the last decade, portfolios with even modest Bitcoin allocations of 1% to 5% have outperformed a traditional 60/40 stock-and-bond portfolio on a risk-adjusted basis.

That is not opinion.

It is math.👇

BlackRock has suggested 1% to 2% of a multi-asset portfolio. Fidelity has modeled 2% to 5%. Galaxy has published research on allocations ranging from 1% to 10%, showing improvements in Sharpe ratios across multiple strategies.

The Bitwise/VettaFi survey backs this up:

among client portfolios that already include crypto, 64% now have allocations greater than 2%, up from 51% in 2024.

The market is moving toward larger, more conviction-driven positions.

Your advisor does not need to agree with those numbers. But they should have a framework for thinking about it: volatility, risk-adjusted returns, tail risk, correlation to existing holdings, and your personal risk tolerance. If the answer is “zero” with no supporting analysis, they are making an emotional decision, not an investment decision.

3. How would you custody crypto, and what are the counterparty risks?

Custody is where theory meets operations.

Ask whether they would use an institutional custodian like Coinbase Prime, Anchorage, Fireblocks, or BitGo.

Ask who holds the private keys.

Ask what happens if the custodian fails.

This is actually the primary concern among wealth managers. They worry about hacks, custody failure, and compliance more than they worry about price volatility.

That concern is valid.

But the landscape has shifted: the SEC rescinded SAB 121 in 2025, opening the door for more banks to offer crypto custody directly. The options are expanding. An advisor’s concern should be producing solutions, not paralysis.

4. How do you handle crypto tax tracking and reporting?

Crypto taxes are genuinely complex.

Cost basis tracking across multiple wallets and exchanges, staking income classification, airdrop treatment, DeFi yield reporting, and the evolving wash sale rules all require dedicated attention.

The EY-Parthenon/Coinbase survey found that 46% of institutional investors cite tax treatment as a top area needing regulatory clarity.

If institutions are wrestling with this, individual holders are flying blind.

If your advisor’s answer is “your CPA will handle it,” that is generally a weak response. However, it’s important to note that your advisor is NOT your CPA and you should always build a specialized team around you for checks, balances, and licensed opinions.

I am not a tax advisor so I won’t answer any questions about tax. BUT… like serious advisors, I have opinions about tracking software, reporting workflows, and how crypto activity integrates with your broader tax picture.

5. What’s your thesis on Bitcoin v. altcoins v. stablecoins?

Here is how I think about it, and your advisor should have a version of this:

Bitcoin serves as a hedged store of value. It is the anchor of any digital asset allocation.

Everything else (the smart contract platforms, the DeFi protocols, the newer tokens) represents speculative bets on technology.

And that is perfectly fine. Speculative bets on technology can offer asymmetric returns. But your advisor needs to understand the difference and have opinions about where the risk-reward sits across these categories.

Stablecoins deserve a separate conversation entirely.

They are not an investment in the traditional sense; they are infrastructure. Stablecoins are settling roughly $800 billion per month, rivaling Visa’s volumes. Your advisor should understand this category as a liquidity and cash management tool, not just another token.

If they treat all crypto as a single undifferentiated bucket, they are not informed enough to manage your exposure.

6. How do you manage risk and drawdowns in a volatile asset class?

Crypto is volatile.

Crypto is risky.

There is a non-zero chance this all goes to zero.

It’s not a secret, and it’s not a disqualifier. But it demands a plan.

Ask about position sizing, rebalancing schedules, cash buffers, and whether they use any hedging strategies. A good advisor does not just pick assets; they build systems around those assets to manage the inevitable drawdowns without triggering panic selling.

7. What would make you change your view on crypto?

This is the meta-question, and it is the most revealing one.

A strong answer references specific data:

adoption metrics,

regulatory developments,

macro liquidity shifts, or

protocol fundamentals.

A weak answer is emotional or ideological.

If your advisor cannot articulate what evidence would move them in either direction, they are operating on conviction rather than analysis.

Conviction without a framework for updating it is just stubbornness.

The Two-Minute Filter

If you want a single question that cuts through everything above, try this one:

“If I gave you $1 million today and wanted 10 percent in crypto, exactly how would you implement it and custody it?”

If they cannot answer that clearly in two minutes, they are not equipped to manage digital asset exposure on your behalf.

Not yet, anyway.

What to Do If Your Advisor Goes 0 for 7

Let me be clear: the answer is probably not “fire your advisor.”

Most financial advisors are excellent at what they do across equities, fixed income, tax planning, and estate strategy. The problem is not competence. It is coverage.

Digital assets are a specialized category that requires dedicated expertise, just like private equity or venture capital. You would not expect your general practitioner to perform surgery. You would ask for a referral.

The same logic applies here.

If your advisor is not equipped to navigate digital assets, ask whether they would be open to collaborating with a specialist who is. An advisor who focuses on digital asset strategy can work alongside your existing team to build a holistic portfolio that accounts for your goals, your risk tolerance, and your existing positions.

The best outcomes come from collaboration, not replacement.

42% of advisors surveyed now believe that late adopters face greater professional risk than early movers face from market volatility. The question is no longer whether crypto belongs in a portfolio conversation. The question is whether the person managing your money is ready to have it.

Ask the seven questions.

The answers will tell you everything you need to know.

Trade carefully out there. Skip the leverage. And if you’re looking for help integrating AI into your advisory practice or building a digital asset framework for clients, you know where to find me.

— Matthew

X: @bit_finance_

oh! one last thing…if you want to dive deeper into how Buffett’s investing principles applies to digital assets, check out my book.

We took 1,300+ pages of wisdom from the Oracle of Omaha and condensed it into a snackable, easy-to-read guide for digital asset investors. Pick up your copy today!

______________

Sources

Bitwise/VettaFi 2026 Benchmark Survey of Financial Advisor Attitudes Toward Crypto

CoinShares, “Inside the Minds of Financial Advisors,” 2025

EY-Parthenon / Coinbase Institutional Investor Digital Assets Survey, January 2025

Galaxy Digital, “The Investable Universe 2.0: Adoption in Motion,” 2025

Matthew Snider is the founder of BitFinance and a principal at Block3 Strategy Group, where he helps organizations and advisors build informed digital asset strategies. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.