What the 2026 Crypto IPO Wave Misses

BitGo rings the bell at the NYSE today and I will be avoiding the IPO like the plague.

And if the rumor mill is accurate, we’ll see Anchorage, and a handful of other crypto infrastructure companies test public markets in the next six months.

The pitch from Wall Street is compelling: these aren’t your 2017 ICOs. These are real businesses with real revenue, regulatory clarity, and institutional backing. The crypto market has matured. Investors are ready.

I’m not buying it. At least not at IPO prices.

The Figma Lesson We’re Already Ignoring

Before we get into crypto, let’s talk about what just happened with Figma.

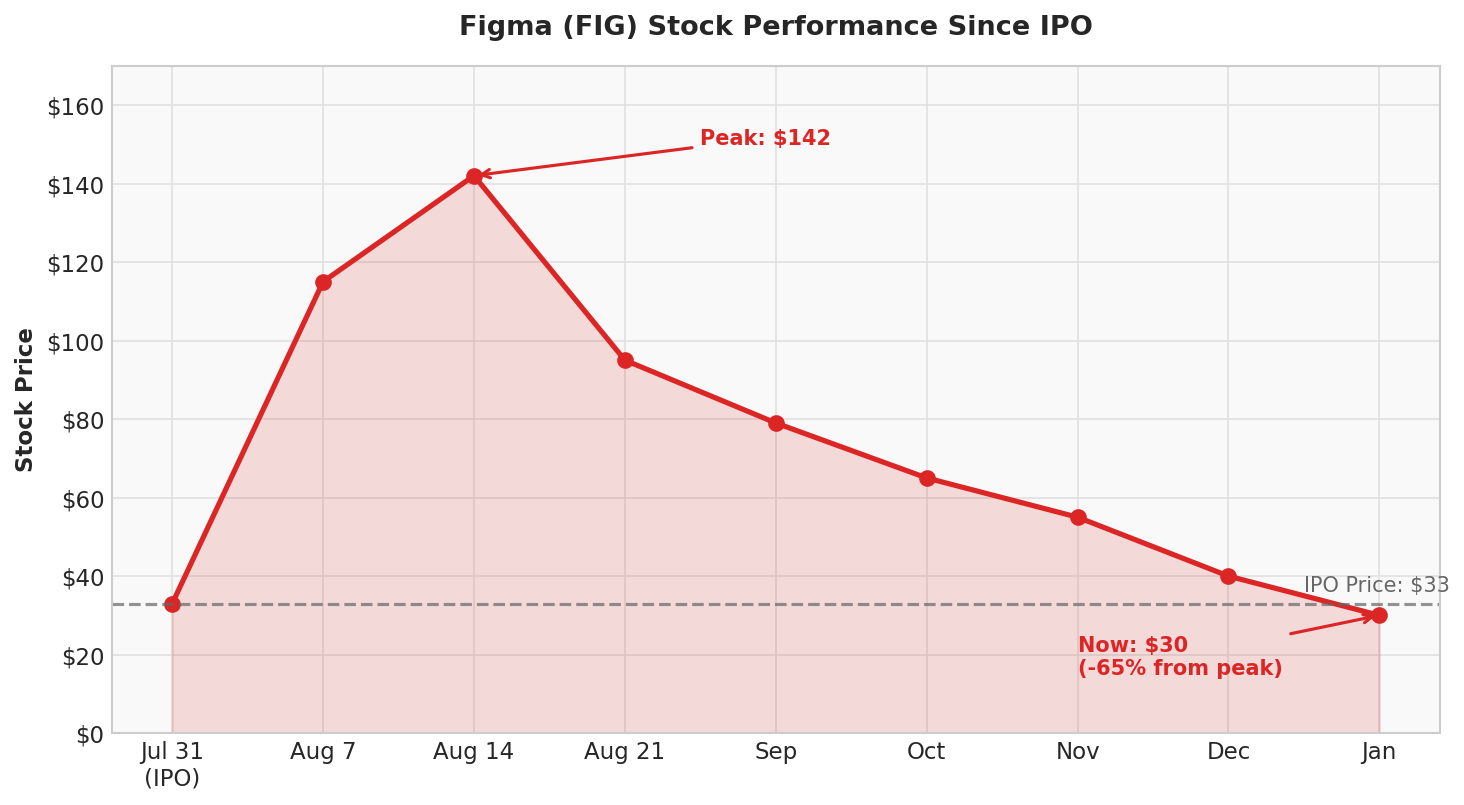

The design software company IPO’d in July 2025 at $33 per share. First day trading? The stock exploded 250% to $115. Retail investors piled in. Social media lit up with celebration posts. Figma hit a peak of $142, giving it a valuation that made Adobe’s failed $20 billion acquisition attempt look like a bargain.

Then reality set in.

Figma’s trajectory from IPO to today tells the whole story.

By mid-August, Figma was trading around $79-82, down more than 55% from its peak. Today it’s hovering near $30, down 65% from the high.

Despite the downtrend, the company’s financials are actually quite strong: 46% year-over-year revenue growth, 91% gross margins. But the initial pricing created expectations that even excellent execution couldn’t support.

This pattern isn’t unique to Figma. Circle, the stablecoin issuer, followed an almost identical trajectory.

The pattern repeats: massive day-one pops followed by steep declines.

Circle IPO’d at $31 in June, jumped 167% on day one to $82, peaked at $298, and is now down roughly 70% from that high.

The math is brutal: if you bought Circle at its peak, you’re sitting on a 70% loss six months later. Yikes.

Why Crypto IPOs Will Follow the Same Script

The dynamics driving Figma and Circle’s volatility are about to repeat themselves with crypto infrastructure companies, but with additional complications.

First, the valuation problem.

We’ve never really seen crypto custodians valued in public markets before. BitGo, Anchorage, and similar companies are pioneering a business model that Wall Street doesn’t have clean comparables for.

How do you value a company that holds digital assets on behalf of institutions?

What’s the margin structure?

What happens to revenue when custody fees compress due to competition?

Nobody really knows how this will play out as a business model long-term.

But that won’t stop investment banks from slapping a valuation on these companies and convincing institutional buyers that the price makes sense.

Proven public companies have track records. Upcoming IPOs are mostly guesswork.

Second, the private market overhang.

Unlike typical IPOs where shares are tightly held by founders and early VCs, many of these crypto companies have broad private market distribution. Accredited investors have been trading shares on secondary markets for years. When the liquidity window opens via an IPO, there’s going to be significant selling pressure from people who’ve been waiting for an exit.

This isn’t speculation.

It’s basic incentives.

If you bought Kraken shares in a secondary transaction at a $10 billion valuation and it IPOs at $20 billion, you’re not holding for the long-term vision. You’re taking the 2x return and moving on.

The ICO Parallel: This dynamic feels a lot like 2017 ICOs. Locked up shares from early investors get dumped on the market at high valuations that retail investors can’t prop up or accurately price. The future is so ambiguous that financials have a hard time proving value with so much uncertainty.

Third, the retail FOMO factor.

Here’s what I observed watching Figma and Circle: retail investors don’t buy these stocks because they’ve done detailed financial analysis.

They buy them because they’re new, they’re trending on social media, and everyone else seems to be buying.

That momentum works both ways. The same retail enthusiasm that drives a stock up 200% can evaporate just as quickly when earnings don’t justify the valuation.

Kraken: The Exception That Proves the Rule

There’s one crypto IPO I’m watching with interest rather than skepticism: Kraken.

Unlike BitGo and Anchorage, Kraken has clear public market comparables. It’s an exchange, just like Coinbase and Robinhood. Analysts know how to value exchanges. They understand the revenue model (trading fees, listing fees, custody revenue). They can look at user metrics, trading volumes, and margin trends.

Kraken has comparables. BitGo and Anchorage are pioneering uncharted territory.

This doesn’t mean Kraken won’t see IPO day volatility. It probably will. But the difference is that after the initial hype settles, there’s a framework for determining what the company is actually worth.

The Four to Six Month Window

Here’s my base case for how this plays out:

These companies will IPO at elevated valuations that reflect private market optimism plus investment banking markup.

Day one will see significant pops as retail investors and momentum traders pile in. Some stocks might double or triple in the first week of trading.

Then the selling pressure begins. Private market shareholders who’ve been waiting years for liquidity start taking profits. Early institutional buyers who got allocation at IPO price sell into the retail enthusiasm. And as the hype fades, people start asking uncomfortable questions about whether a $2 billion valuation for a custody business makes sense.

The playbook: avoid the danger zone, wait for the opportunity zone.

Four to six months post-IPO, I expect most of these stocks to be trading 30-50% below their peaks. Maybe more if we hit any broader market turbulence or crypto-specific headwinds.

That’s when I’ll start paying attention.

What I’m Doing Instead

If you’re interested in exposure to crypto infrastructure but don’t want to play the IPO game, here are the alternatives I’m considering:

Proven public companies. Coinbase and Robinhood have already been through the IPO cycle. They’ve reported multiple quarters of earnings. You can evaluate them based on actual performance rather than projections. They’re not as exciting as brand new IPOs, but excitement isn’t always profitable.

Traditional companies using blockchain. Visa, Mastercard, and companies like Avery Dennison are integrating blockchain technology into existing business models. You’re not betting on pure-play crypto adoption. You’re betting on established companies adding incremental revenue through new technology. Lower upside, but much lower risk.

Waiting for the washout. Sometimes the best trade is no trade. If I’m right about the four to six month cycle, there will be opportunities to buy these companies at much more reasonable valuations once the initial hype fades and sellers have exhausted themselves.

The Bottom Line

I’ve seen this movie before. Not just with crypto, but with every hot sector that Wall Street decides to package and sell to retail investors. The first movers rarely win. The patient buyers do.

BitGo, Kraken, and Anchorage might all be excellent businesses with real long-term potential. But excellent businesses can still be terrible investments if you pay the wrong price.

So I’m sitting this one out. At least for now.

If you disagree or if you’re planning to buy into any of these IPOs, I genuinely want to hear your reasoning. Reply to this email or leave a comment. Maybe I’m missing something. Maybe there’s a case for buying at IPO prices that I haven’t considered.

But based on what I’ve seen in the last six months with Figma and Circle, I’m betting that patience will be rewarded.

We’ll check back in six months and see who was right.

Not investment advice. Do your own research. Past performance doesn’t guarantee future results. All the usual disclaimers apply.

— Matthew

X: @matthew_mba_

oh! one last thing…I mentioned the book above:

We took 1,300+ pages of wisdom from the Oracle of Omaha and condensed it into a snackable, easy-to-read guide for digital asset investors. Pick up your copy today!