I Spent 3 Days on a Beach with 600 Advisors; Here’s Where the Money Is Moving.

Every year, FutureProof brings a few hundred advisors, allocators, and technology vendors to Miami Beach for three days of structured meetings and unstructured conversation. It’s not a keynote conference. It’s closer to a three-day partner dinner where you actually learn what people are thinking, building, and worrying about.

I went so you didn’t have to.

Here’s what stood out.

These aren’t conference talking points. They’re the themes that kept surfacing across 20 separate, intentional meetings with independent advisors, fund operators, and AI vendors. If you’re allocating capital, advising clients, or building products in the wealth management space, these are the signals worth paying attention to.

1. AI + Adviser = Fiduciary Upgrade (Not Replacement)

This was the conference’s clearest consensus.

There was an entire AI pavilion showcasing tools built specifically for financial advisors, and almost none of them were trying to replace the human in the room.

The focus was overwhelmingly on making the adviser’s workflow better: smarter meeting prep, faster compliance review, more personalized client communication. Better user experience, not better stock picks.

By The Numbers

78% of wealth management firms actively seeking agentic AI opportunities.

57% of RIAs already use AI tools, with another 29% exploring adoption.

93% of advisors say they want to maintain control over AI outputs.

Only one or two organizations were actually building tools to help people make better investment decisions. That’s a meaningful distinction.

The industry has, at least for now, landed on a position: AI makes the adviser more valuable, not less. The framing that resonated most was that AI plus a human adviser equals a fiduciary upgrade. The alternative framing, that AI replaces the adviser, still feels more like a liability conversation than an opportunity conversation.

Munger would probably say this is rational. Clients don’t just need data. They need someone to sit with them when markets are ugly and help them not do something stupid. AI can’t do that part yet. Maybe it never will.

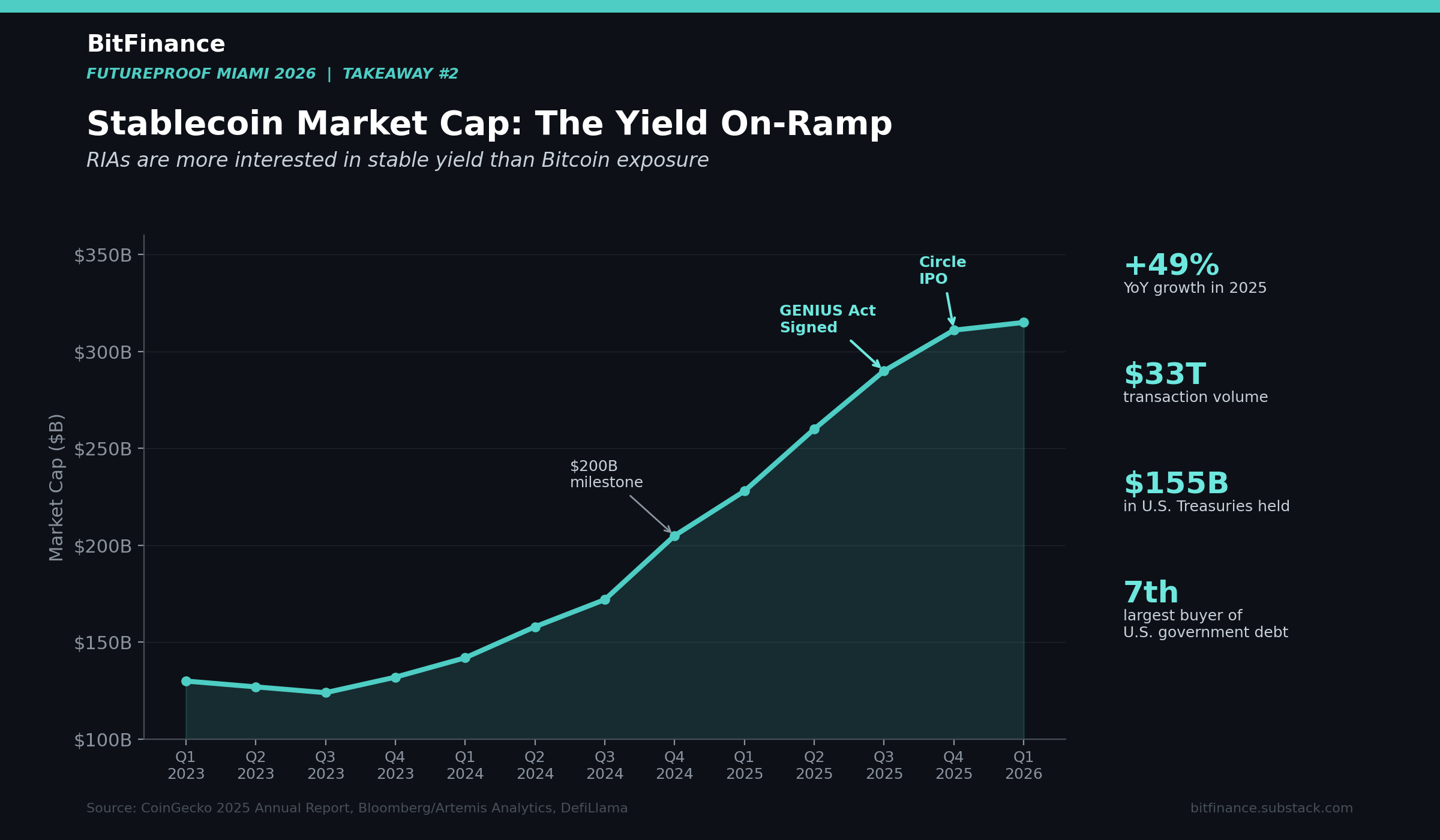

2. Stablecoin Yield Is the On-Ramp RIAs Actually Want

Crypto had a smaller footprint at FutureProof than last year.

No Michael Saylor.

No Matt Hougan.

Fewer big-name sponsors from the digital asset world.

But here’s what caught my attention: in 20 separate meetings, very few people expressed interest in Bitcoin or altcoins specifically. What they were interested in was yield. Predictable, stable, boring yield. And increasingly, stablecoins are delivering exactly that.

The pitch that’s actually working with RIAs isn’t “buy Bitcoin.” It’s “what if your clients could earn better than money market rates through a digital dollar product, without the volatility of holding crypto?” That reframe changes everything.

The advisors I spoke with are far more willing to explore a stable yield product than to have the Bitcoin conversation with their compliance department. It removes the emotional baggage of crypto and replaces it with something their clients already understand: yield on cash.

The numbers support why this is gaining traction. Stablecoin issuers are now among the largest holders of U.S. Treasuries. The GENIUS Act, signed last year, gave the sector its first federal regulatory framework. Circle just went public. Visa’s stablecoin-linked card spend hit a $4.5 billion annualized run rate.

This isn’t a side project anymore. It’s becoming real financial infrastructure.

Banks and traditional institutions can essentially sidestep the entire crypto stigma by saying they offer a “digital dollar that provides yield.” The underlying technology is blockchain. The regulatory wrapper is clear. The client comfort is night and day.

Whether you view that as bullish or cynical probably depends on how much you care about labels versus outcomes. But for the adviser sitting across from a skeptical client, this framing is a gift.

3. Private Credit Is the Room’s Biggest Question Mark

Private credit was well-represented in the exhibit space. Lots of products, lots of pitch books. But in the conversations behind closed doors, the tone was more cautious. People weren’t dismissing private credit. They were asking better questions about it. How are these loans being valued? Who’s marking them? What happens when the music slows down?

Those are the right questions. The high-profile bankruptcies of Tricolor and First Brands in late 2025, combined with Jamie Dimon’s warning that credit problems are rarely isolated, have shifted the mood. This isn’t panic. But the room’s relationship with private credit has evolved from uncritical enthusiasm to something more measured. The product shelf is crowded. The due diligence is tightening. That’s probably healthy.

By the numbers:

Investors pulled $7 billion+ from the largest private credit funds in Q4 2025.

Private credit AUM is expected to exceed $2 trillion in 2026.

Morningstar has warned about worsening credit profiles among both high- and low-quality borrowers heading into 2026.

Buffett has always been clear about this: when the tide goes out, you find out who’s swimming naked. Private credit hasn’t had a real stress test yet. The advisors in this room seemed aware of that.

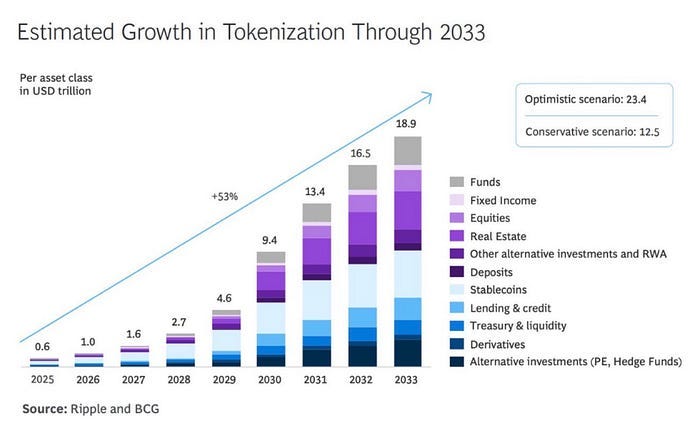

4. Tokenization Has Quietly Leapfrogged “Bitcoin Adoption”

Here’s something that would have surprised me two years ago: in a room full of advisors, the word “tokenization” generated more genuine curiosity than “Bitcoin.” People weren’t asking about price. They were asking about infrastructure. How does a tokenized treasury work? What does it mean for settlement? Can I use this in a client portfolio?

That shift is significant.

If stablecoin yield is the on-ramp for cash management, tokenization is the on-ramp for everything else. It takes the most useful parts of blockchain technology, faster settlement, fractional ownership, transparent record-keeping, and wraps them in language that doesn’t trigger the same allergic reaction that “crypto” does. BlackRock’s BUIDL fund, Franklin Templeton’s on-chain money market fund, JPMorgan’s tokenized collateral network.

These aren’t experiments anymore. They’re products with real AUM.

For advisors still on the fence about digital assets, tokenization may be the conversation that finally makes sense to their compliance department. It doesn’t ask you to believe in Bitcoin. It asks you to believe in better financial plumbing. That’s a much easier sell.

5. Bitcoin in Annuities Is the Trend Nobody Is Talking About

I spoke with someone in the annuities space who had no idea that Bitcoin-linked annuity products existed. None. And this is a person whose entire livelihood depends on knowing what’s happening in that market.

That gap is the opportunity. The U.S. annuity market is enormous, and the idea that you can now offer principal-protected exposure to Bitcoin through a fixed index annuity, through BlackRock no less, is a structural shift that most advisors haven’t processed yet. The product gives retirees upside participation in Bitcoin without putting their principal at risk. That’s a sentence that would have been absurd three years ago.

Corebridge has already followed with its own version, working with Invesco. This isn’t one company experimenting. It’s the beginning of a product category. And it’s happening inside the most conservative product wrapper in all of wealth management: the annuity.

By the numbers:

Delaware Life and BlackRock launched the first fixed index annuity with Bitcoin exposure in January 2026, blending 74% S&P 500 exposure with 25% IBIT allocation at a 12% target volatility.

Corebridge Financial followed with a separate Bitcoin-linked annuity through Invesco. Meanwhile, a Bitcoin-native life insurer, has raised $122 million to scale BTC-denominated retirement products. U.S. annuity sales hit record highs in 2025.

If you’re an adviser and your clients have exposure to annuities, this is worth understanding now. Not because every client needs it. But because the conversation is coming, and the advisers who can speak to it intelligently will have a meaningful advantage over those who can’t. The people building these products are betting that the demand is there. The annuity professionals I met at FutureProof didn’t even know the supply existed. That disconnect won’t last.

The Bigger Picture

If there was one meta-theme across all of these conversations, it’s this: the industry is getting more comfortable with new tools and less comfortable with old assumptions. AI is being welcomed, but with guardrails. Stablecoins are gaining ground because they deliver yield without the volatility baggage. Private credit is being scrutinized more carefully. And the advisors who are leaning into education, not just products, are the ones their clients trust most.

We’re still early. That’s not a crypto talking point. It’s a statement about the pace of structural change in how wealth is managed, allocated, and protected.

The technology is outpacing the comfort level.

But the gap is closing.

- Matthew

X: @bit_finance_

The best investors I know got that way by reading widely and talking to the right people.

If BitFinance belongs in someone’s inbox, send it their way.

Referrals unlock free PDFs, paid access, and more.

oh! one last thing…if you want to dive deeper into how Buffett’s investing principles applies to digital assets, check out my book.

We took 1,300+ pages of wisdom from the Oracle of Omaha and condensed it into a snackable, easy-to-read guide for digital asset investors. Pick up your copy today!

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.

Sources

EY-Parthenon, “GenAI in Wealth & Asset Management Survey 2025” (January 2026). 78% of firms actively identifying agentic AI opportunities; compliance and risk management realizing largest cost savings.

Schwab, “2025 Independent Advisor Outlook.” 57% of RIAs use AI tools today, with another 29% exploring how to get started.

Advisor360°, “2026 Connected Wealth Report: AI Edition” (January 2026). Survey of 301 U.S. financial advisors. 93% want control over AI outputs; 74% say AI is an advantage; 46% lack confidence in AI outputs.

CoinGecko, “2025 Annual Crypto Industry Report” (January 2026). Stablecoin market cap surged 48.9% in 2025, adding $102.1 billion to reach $311 billion.

Bloomberg, citing Artemis Analytics. Stablecoin transaction volume rose 72% in 2025 to $33 trillion.

Stablecoin Insider, “50 Stablecoin Statistics That Matter in 2026” (January 2026). Issuers held approximately $155 billion in U.S. Treasury bills by October 2025. Visa stablecoin settlement volumes hit $4.5 billion annualized run rate as of January 2026. Stablecoin-based B2B payments surged from under $100 million monthly in early 2023 to over $6 billion by mid-2025.

Financial Times, Q4 2025 reporting. Investors pulled more than $7 billion from the largest private credit funds in the fourth quarter of 2025.

Moody’s, “Private Credit Outlook 2026” (January 2026). AUM expected to exceed $2 trillion in 2026.

With Intelligence, “Private Credit Outlook 2026” (March 2026). When selective defaults and liability management exercises are included, the “true” default rate approaches 5%.

Goldman Sachs. Approximately $220 billion of assets in retail-focused evergreen private credit funds, representing roughly 20% of total lending exposure.

Morningstar. Warning about worsening credit profiles among both high- and low-quality borrowers in 2026.

RWA.xyz (March 2026). Tokenized real-world assets (excluding stablecoins) surpassed $26.55 billion distributed on-chain, with 667,637 total asset holders.

CoinDesk Research, “Digital Assets 2026: Above the Noise” (February 2026). Total value locked across RWA protocols surged 210% to $22.8 billion since 2025.

McKinsey. RWA tokenization market projected to reach $2 trillion by 2030.

BlackRock / Delaware Life (January 2026). Launch of the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index on three Delaware Life fixed index annuity products. 74% iShares Core S&P 500 ETF, 25% iShares Bitcoin Trust ETF (IBIT), 1% cash.

Corebridge Financial / Invesco. Launch of a separate Bitcoin-linked index annuity via the Invesco QQQ ETF and Invesco Galaxy Bitcoin ETF (BTCO).

CoinDesk (October 2025). Meanwhile, a Bitcoin-native life insurer, raised $82 million (total raised: $122 million) to scale BTC-denominated retirement products. Regulated by the Bermuda Monetary Authority.