The Dalio Myth

Last week, Ray Dalio published an essay titled “It’s Official: The World Order Has Broken Down.” Within hours, finance Twitter was treating it like required reading. LinkedIn was awash with praise. One prominent crypto influencer called it “the most important thing you’ll read this year.”

I read it too. It was well written. It was thought-provoking. And it prompted me to do something that apparently very few people bother to do before amplifying Dalio’s work.

I checked his scoreboard.

What I found is worth your time, whether you agree with my conclusions or not. Because the gap between Dalio’s reputation and his results raises questions that anyone allocating capital, or consuming his analysis, should be asking.

The Numbers That Nobody Talks About

Let’s start where it matters most for anyone in finance: performance.

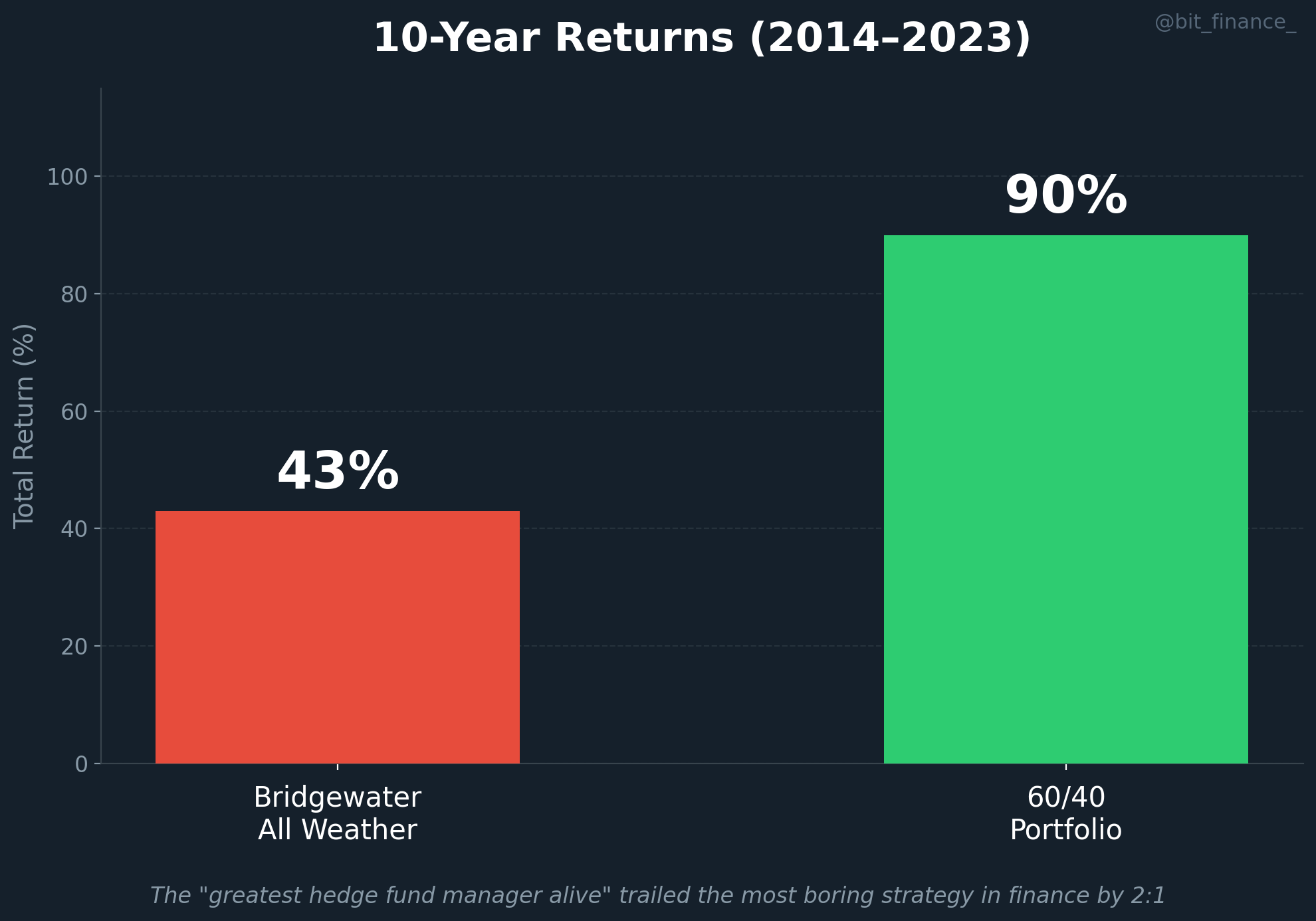

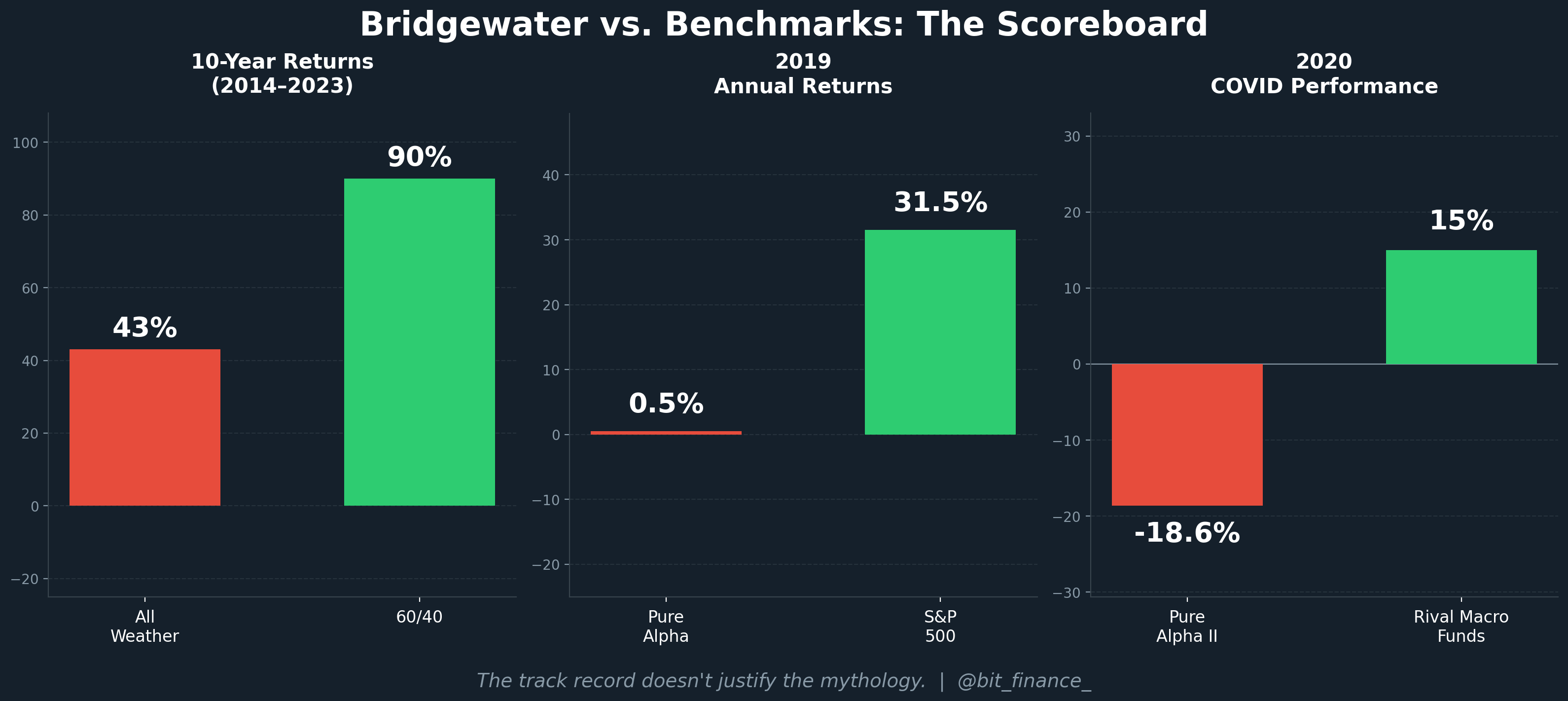

For the 10-year period from 2014 to 2023, Bridgewater’s All Weather fund returned 43%. During the same window, a standard 60/40 portfolio returned 90%.

That is not a marginal gap.

A simple, passive allocation strategy that requires no proprietary system, no team of PhD quants, and no multi-billion dollar infrastructure outperformed the world’s largest hedge fund by a factor of nearly two to one.

It gets more specific.

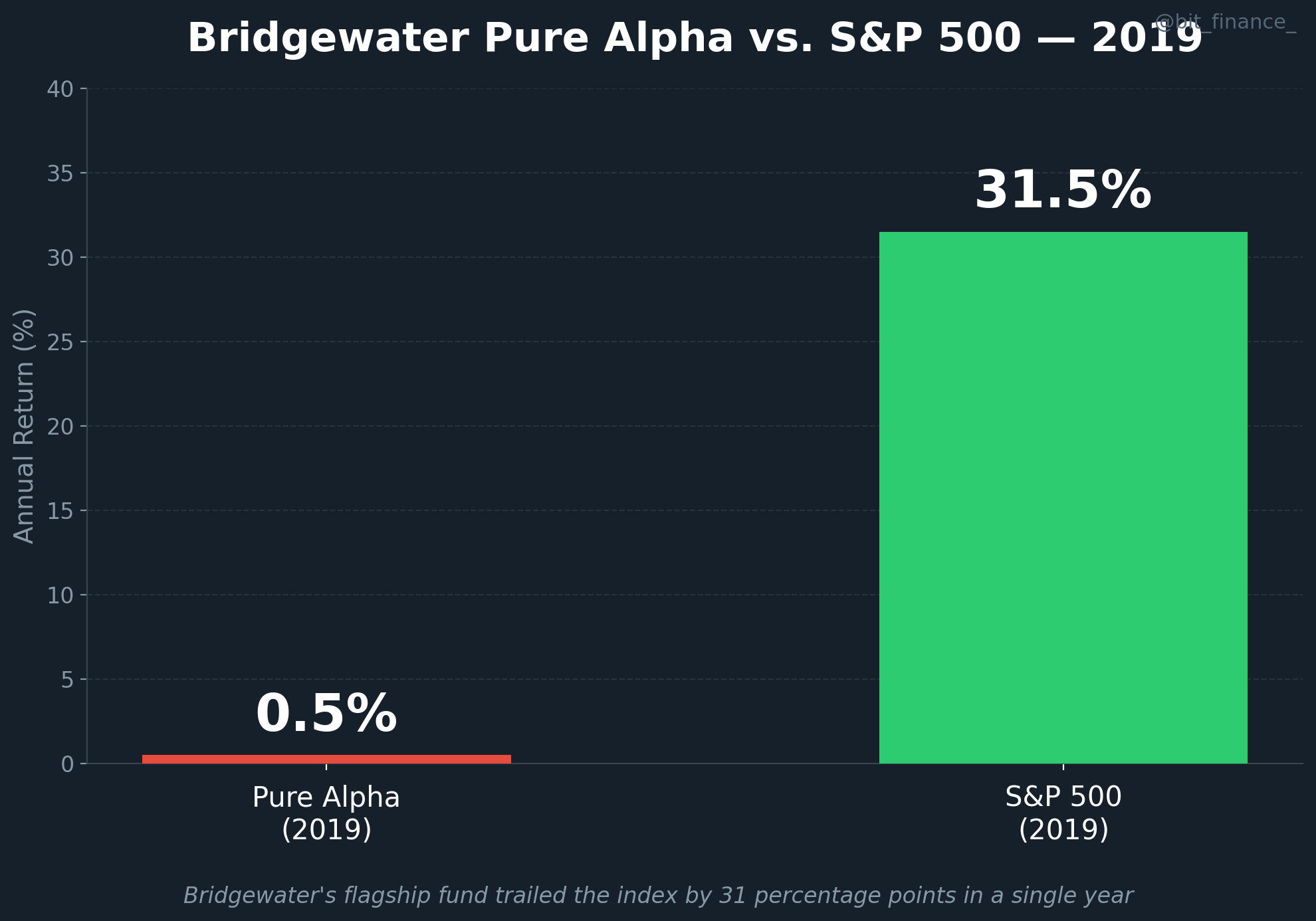

In 2019, Bridgewater’s flagship Pure Alpha fund returned approximately 0.5%.

That same year, the S&P 500 gained 31.5%.

You could have bought a low-cost index fund at any point that year and outperformed one of the most celebrated investment vehicles in history by 31 percentage points.

In 2020, Pure Alpha II lost 18.6% during COVID volatility, contributing to $12.1 billion in total losses. This is notable because macro hedge funds are supposed to thrive in volatile environments. That is their entire value proposition.

Yet rival macro funds like Caxton and Brevan Howard posted double-digit gains in the exact same conditions.

The annualized underperformance relative to a basic index approach was roughly 3%, with approximately 2% attributable to fees. And the institutions absorbing those fees were not family offices or high-net-worth individuals looking for a thrill.

They were pension funds and endowments.

Teachers.

Firefighters.

University students.

A 2023 New York Times investigation added another layer of complexity, raising questions about whether Bridgewater’s “sophisticated investing system” even existed as marketed.

The reporting suggested that the fund’s returns were primarily driven by Dalio’s personal picks and relationships with prominent government actors, not the systematic, rules-based process that was presented to institutional allocators.

I want to be clear about something. I am not arguing that Dalio lacks intelligence. He clearly does not. What I am suggesting is that intelligence and branding should not override a decade of data when real people’s retirement security is at stake.

The Culture Behind the Curtain

Dalio built his public persona around “radical transparency,” a framework where the best ideas win regardless of hierarchy, everyone is rated, and ego is checked at the door. His book Principles became a management philosophy that corporate leaders across industries tried to emulate.

The internal reality, as documented by multiple investigations and former employees, tells a different story.

Employees at Bridgewater were subjected to public “trials” where their alleged faults were detailed in front of hundreds of coworkers. These sessions sometimes ended in on-the-spot firings.

All of them were recorded and stored in files that any employee could access and review.

In one particularly notable episode, Dalio reportedly had a video produced of a female employee’s emotional breakdown after he berated her about a hiring issue. According to reporting from The Daily Beast, he screamed at her, waited for her lip to quiver, then screamed again for failing to control her emotions.

The video was distributed company-wide. Prospective job candidates were made to watch it during the interview process.

Here is the detail that sticks with me the most:

Dalio rigged Bridgewater’s computerized employee rating system so that he was the only person excluded from being rated.

In a culture built entirely on the premise that everyone is accountable to the same standard, the architect exempted himself.

Charlie Munger once said that you should never trust anyone who doesn’t have skin in the game. I think about that a lot when I read Principles.

James Comey, the future FBI director, served as Bridgewater’s general counsel at a reported $7 million per year. Among his responsibilities: conducting a formal investigation into an employee who failed to bring bagels on the agreed-upon day, and designing entrapment schemes where binders were left out to see if employees would open them. I wish I were making this up.

Cameras monitored everything. Employees were encouraged to report on colleagues. Some staff reportedly removed batteries from company-issued cell phones when spending time with family and friends. Departing employees faced two years of unpaid gardening leave during which they needed permission to take a new job.

This is the culture that half of corporate America attempted to replicate after reading Dalio’s book. It is worth asking whether they knew what they were actually copying.

The China Problem

When asked on CNBC about China’s human rights violations and how they factored into his investment strategy, Dalio said he “can’t be an expert in those types of things” and had “really no idea.”

This is worth pausing on.

Dalio’s been traveled to China since 1984. He is widely regarded as one of the most sophisticated macro investors alive. His “Changing World Order” framework is built on geopolitical analysis spanning centuries and civilizations.

And he can’t be an expert on China’s human rights record.

It is also relevant to note that Bridgewater had become one of the largest foreign private fund managers in Beijing, having raised a $1.25 billion Chinese fund.

The incentive structure here is not complicated. When your fund depends on access to CCP-controlled capital markets, your public commentary about the CCP will reflect that dependency.

Dalio told investors not to view China’s tech crackdown as anti-capitalist, even as Beijing was dismantling entrepreneurs like Jack Ma and forcing Ant Group to scrap its IPO. Economists with genuine expertise in the region called him flat-out wrong, noting that his business interests made him a compromised commentator.

He also expressed what I would call a revealing sentiment about governance: he said publicly that he was “scared of ‘one man, one vote’ because it suggests that everyone has an equal ability at making decisions.”

I think you learn a lot about a person’s framework by examining what they say when they believe they are among friends.

The Self-Mythology

Every successful investor cultivates a narrative.

That is part of the job.

But there is a meaningful difference between building a reputation and constructing an alternate reality.

Dalio compared himself to both the Dalai Lama and Steve Jobs. He had his team pitch his biography to Walter Isaacson, Jobs’s biographer. Per Rob Copeland’s extensive reporting, Dalio has been “distorting reality in a major way for years,” and current Bridgewater leadership allegedly knows the public image is a fabrication.

Even the philanthropic narrative has complications. Dalio’s $100 million education partnership with Connecticut was disbanded after just over a year amid mismanagement charges. The former CEO alleged she was made a scapegoat and that Dalio told her not to draw on her own accumulated expertise, but to take direction from his wife Barbara instead.

Legendary AI scientist David Ferrucci, the architect of IBM Watson, was reportedly hired under the impression he would work on economic modeling. He was instead put to work building an app version of Principles.

I have nothing against confidence, or even ego when it is earned. But there is a threshold beyond which self-promotion becomes something else entirely. And I think a reasonable person reviewing the available evidence would conclude that threshold was crossed some time ago.

Why This Matters…

I am writing this piece because I think our industry has a recurring blind spot, and it has real consequences.

When institutions allocate capital to Bridgewater based on Dalio’s reputation rather than a rigorous evaluation of recent performance, the beneficiaries of those institutions pay the cost.

This is not abstract.

These are defined benefit pension plans. University endowments. Public employee retirement systems.

When millions of professionals read Principles and try to implement “radical transparency” without understanding what it actually looked like inside Bridgewater, they risk creating environments that harm people while believing they are doing something aspirational.

And when we collectively treat Dalio’s geopolitical commentary as essential reading without examining the business interests that may shape his analysis, we are outsourcing our critical thinking to someone who has significant financial incentives to frame certain conclusions in a particular way.

I have spent much of my career thinking about governance, incentives, and the gap between how investment products are marketed versus how they actually perform.

The Dalio story is a case study in all three.

The Uncomfortable Conclusion

Ray Dalio wrote a bestselling book about principles he did not follow. He built a culture of accountability that he exempted himself from. And he delivered a decade of returns that a retiree with two index funds and a free afternoon could have outperformed.

The world order may or may not be breaking down. I will leave that to better geopolitical minds than mine.

But the Dalio myth? I think the scoreboard speaks clearly enough.

As Buffett himself once said: when the tide goes out, you see who’s been swimming naked.

Maybe it’s time we checked the beach.

Trade carefully out there. Skip the leverage. And if you’re looking for help integrating AI into your advisory practice or building a digital asset framework for clients, you know where to find me.

Until next week.

— Matthew

X: @bit_finance_

oh! one last thing…if you want to dive deeper into how Buffett’s investing principles applies to digital assets, check out my book.

We took 1,300+ pages of wisdom from the Oracle of Omaha and condensed it into a snackable, easy-to-read guide for digital asset investors. Pick up your copy today!

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015.

Sources: CAIA Association (All Weather performance), Institutional Investor (Pure Alpha 2019), The Daily Beast (workplace culture), Rethinking65 (rating system, workplace practices), Newsweek (China commentary), CNBC (China tech crackdown), Jacobin (democracy comments, self-comparisons), Axios (Ferrucci, NYT investigation), Fox Business (Connecticut partnership), WHYY (NDAs, harassment allegations), Fortune (model updates), Postshift (Murray departure), Wikipedia (Bridgewater performance history)