The One-Syllable Thesis: What Prediction Markets Teach Us About How Decisions Actually Get Made

I need to tell you about the dumbest investment thesis I’ve ever heard.

It made someone six figures.

The JD Vance Theory

During a 60 Minutes interview, a prominent, high-stakes user known as “Domer” explained how he turned roughly $5,000 into $250,000 betting that Trump would pick JD Vance as his VP.

His research methodology? He read somewhere that Trump really likes people whose last names he can pronounce easily. Specifically, names that are one syllable.

Vance. One syllable.

That was the thesis. That was the whole thing.

Not policy alignment. Not donor relationships. Not swing state appeal. Not any of the things that political analysts spent months debating on cable news.

Just: can Donald Trump say your name without thinking about it?

I laughed when I heard this. Then I stopped laughing. Then I put money on Kevin Warsh.

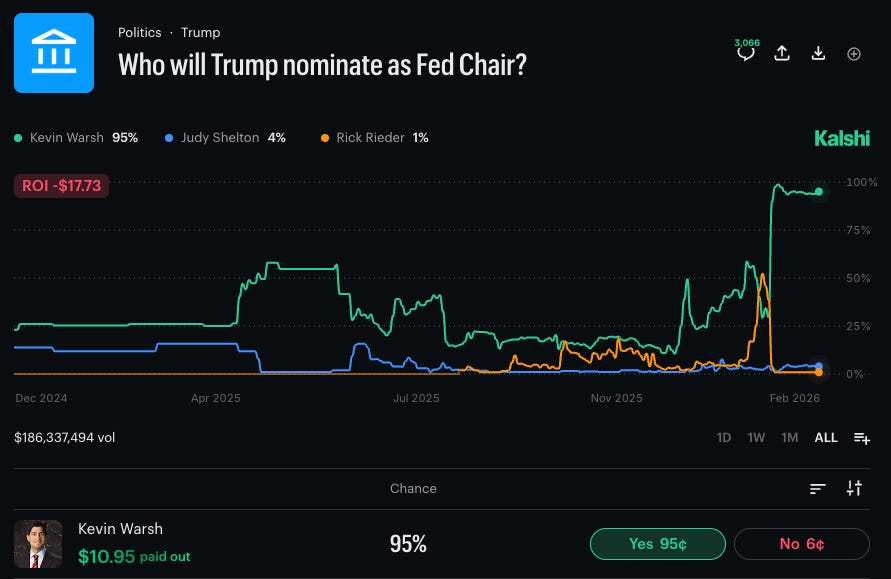

The Warsh vs. Bessent Question

For months, the prediction markets have been pricing in who Trump would nominate for Treasury Secretary. The two front-runners were Kevin Warsh and Scott Bessent.

Both qualified. Both connected. Both with legitimate credentials for the role.

But here’s the thing.

Warsh. One syllable.

Bessent. Two syllables.

I’m not saying this is rigorous analysis. I’m saying I’ve had money on Warsh this entire time, and the reasoning is exactly as stupid as it sounds.

This is what prediction market research looks like now. We’re not evaluating whether someone will be good at the job. We’re evaluating whether the person making the decision can pronounce their name without pausing.

And somehow, it keeps working. I placed my (modest) bet in early January when Warsh’s probability to be nominated was about 40%.

Sadly, we are not retired…yet.

The Trump Speech: 16 Out of 18

Let me give you a more recent example of how these markets actually move.

Polymarket runs bets on what words Trump will say during speeches. Before a recent address made around MLK Day, you could bet on whether he’d mention specific terms: “tariffs,” “China,” “beautiful,” “tremendous,” whatever list they put together.

Trump mentioned 16 out of 18 words on the list.

If you had placed bets on all 18, you would have hit 89% of them. Not because you’re a genius. Because Trump is predictable. He has themes. He has favorite words. He goes off script in consistent directions.

The edge isn’t in knowing something secret. The edge is in recognizing that certain people behave in patterned ways, and betting accordingly.

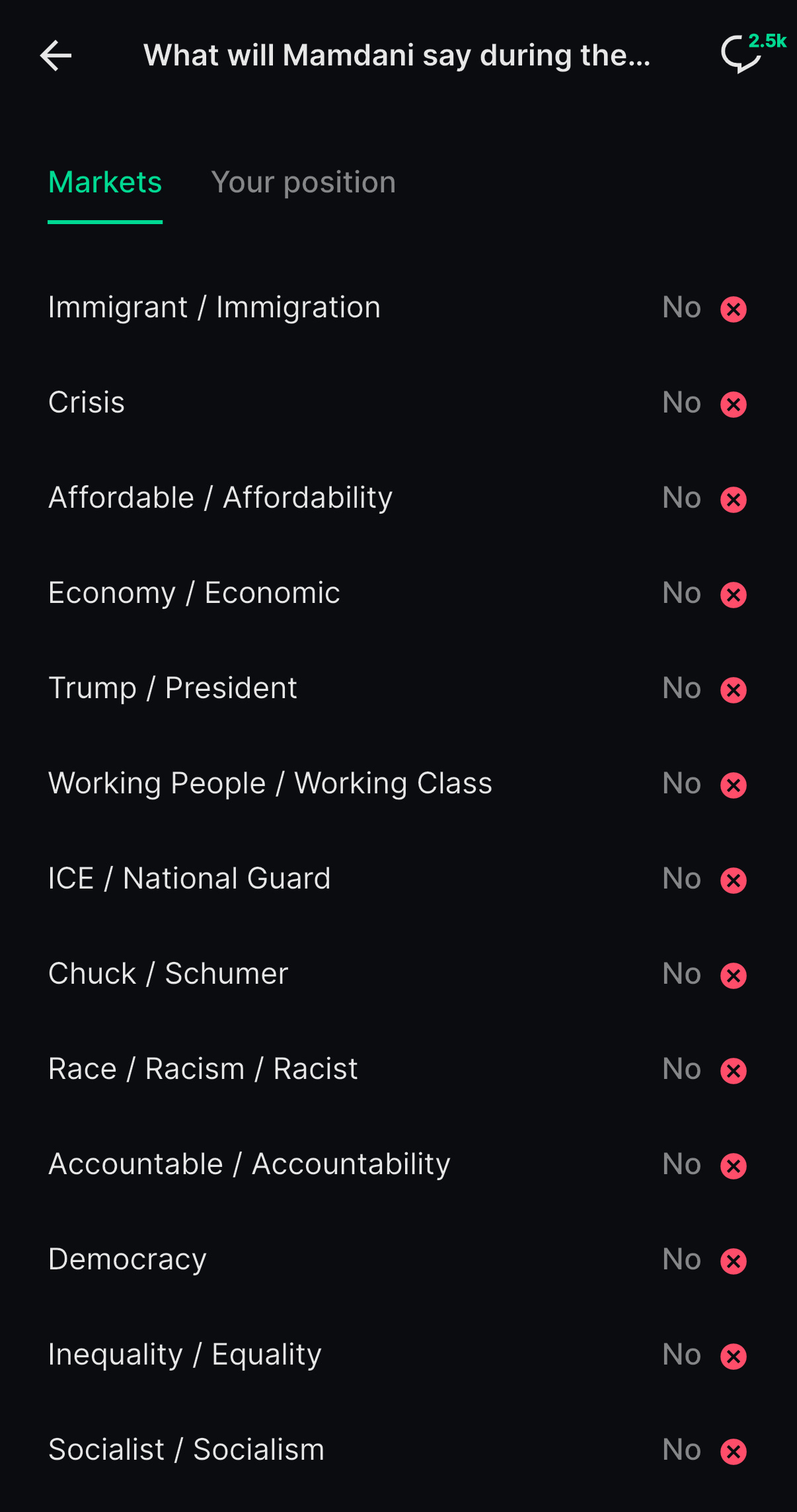

The Mamdani Speech: Zero Out of Thirteen

Now here’s where it gets interesting.

The same week, Polymarket ran a similar bet on a speech by V. Mamdani, New York City’s Deputy Mayor, on MLK Day.

He mentioned zero out of 13 words on the list.

Zero.

If you had bet “no” across the board, betting that he would NOT say any of the predicted terms, you would have hit 100% of your positions. Every single one resolved in your favor.

Now, I have no idea if Mamdani knew about the Polymarket bets. Probably not. But the contrast is striking.

Trump: 16 out of 18 resolved to “Yes”

Mamdani: 0 out of 13 yeses. Which means 13 out of 13 resolved to “No”.

One person is maximally predictable. The other is either intentionally unpredictable or just operating on a completely different wavelength than the market expected.

Both patterns are tradable if you see them.

The Uncomfortable Question

Here’s what makes prediction markets fascinating and slightly uncomfortable at the same time.

Some of this feels a lot like insider trading.

If you know Trump’s speech prep. If you know who he’s been talking to. If you know what topics are on his mind because you’re in the room. You can print money on these bets.

The same dynamics that make stock trading on material non-public information illegal are just... completely fine in prediction markets. At least for now.

I’m not saying people are cheating. I’m saying the incentive structures are wild, and the edges come from places that would get you arrested in traditional finance.

When a Polymarket whale drops $30 million on an election outcome, nobody asks where the conviction came from. We just assume they did “research.”

Maybe they did. Maybe research looks different than we thought.

What This Actually Teaches Us

Strip away the prediction market stuff for a second.

The deeper point is about how decisions get made by powerful people.

We assume that major appointments, policy choices, and strategic moves are the result of careful deliberation. Meetings. Memos. Analysis.

Sometimes they are.

But sometimes the deciding factor is whether someone’s name is easy to say. Or whether they were in the room at the right moment. Or whether the decision-maker just likes them.

The JD Vance thesis sounds ridiculous until you realize it captured something true about how Trump makes choices. Not the official criteria. The actual criteria.

Prediction markets, at their best, force you to bet on how the world actually works rather than how it’s supposed to work.

That’s a different skill than traditional analysis. And honestly, it might be more valuable.

The Takeaway

I don’t know if Kevin Warsh will get nominated for Fed Chair or whatever role comes next. The one-syllable thesis is not financial advice.

But I’ve stopped dismissing the “dumb” theories.

The question isn’t whether an investment thesis sounds sophisticated. The question is whether it captures something true about how the decision-maker actually thinks.

Sometimes that’s policy papers and donor networks.

Sometimes it’s syllable counts.

The prediction markets don’t care which one. They just pay out based on what happens.

— Matthew

X: @bit_finance_

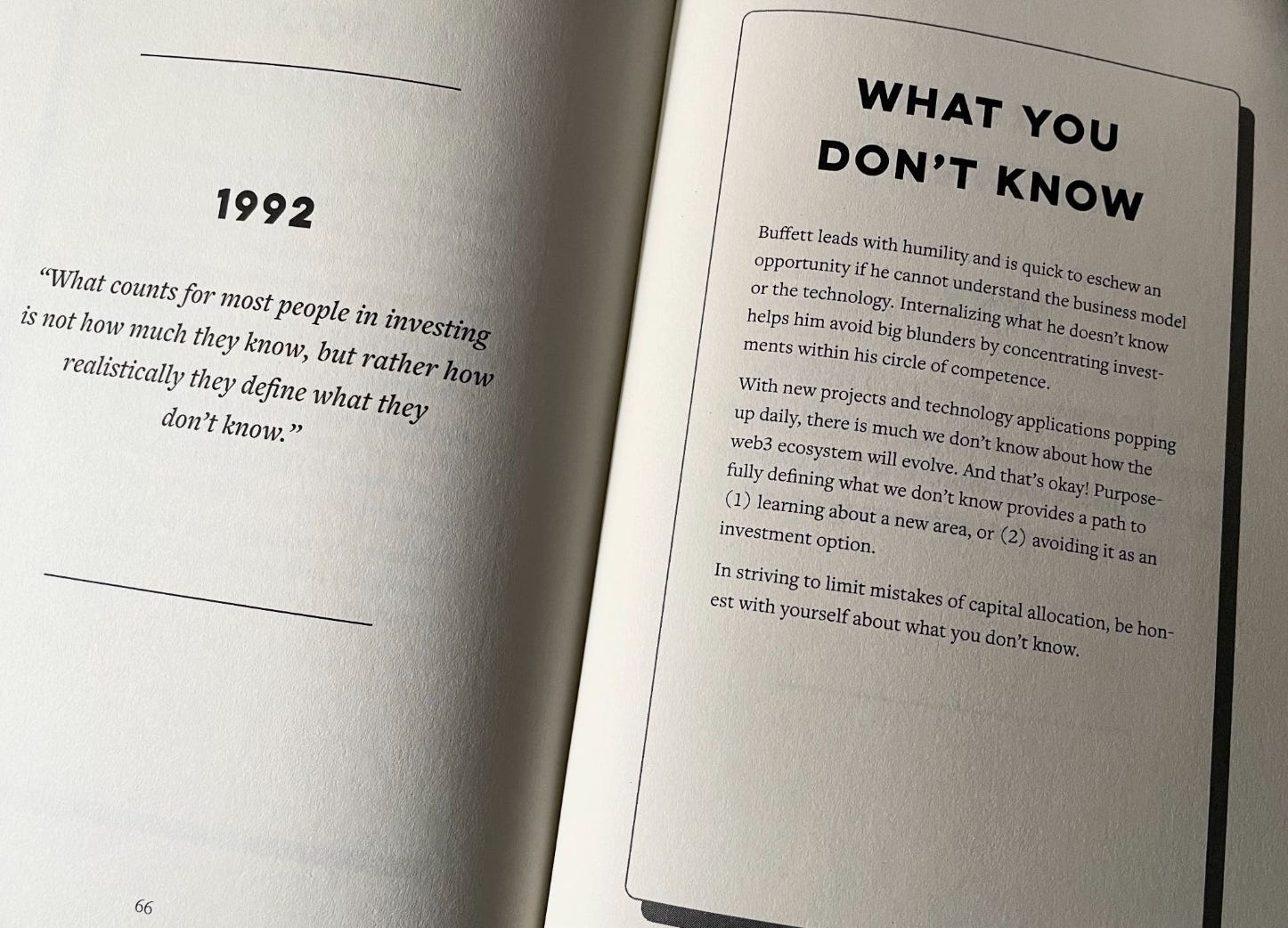

oh! one last thing…if you want to dive deeper into how Buffett’s investing principles applies to digital assets, check out my book.

We took 1,300+ pages of wisdom from the Oracle of Omaha and condensed it into a snackable, easy-to-read guide for digital asset investors. Pick up your copy today!

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.